Media reports of the government offloading a substantial chunk of its shareholding in IDBI Bank to Life Insurance Corporation of India (LIC) has sparked off another round of passionate debate on the appropriateness of the action. To be sure, LIC has been an equity investor of last resort for the government for many years — periodically picking up the slack in capital market sentiments for the government’s interventions. Primarily, this has been around the disinvestment programme, with LIC consistently bailing out share sales in PSUs with lukewarm investor interest (a recent case in point being the Hindustan Aeronautics Ltd (HAL) IPO).

One objection to this has been a purists’ lament around whether such share sale really means “disinvestment” of government equity. However, the bigger and arguably a more pertinent point is around whether LIC is being amiss in its fiduciary responsibility as an insurer by deploying capital in sub-par investments, just to bail out the government. IDBI Bank, with its stressed balance sheet (28% gross NPA), is symptomatic of such “subpar investments”. The latter argument has strong merit — the capital available with LIC is essentially premia paid by its policyholders. LIC invests this capital in order to generate enough surpluses to fund claims, death benefits and maturity proceeds to policyholders and their beneficiaries. To the extent LIC makes sub-optimal investment decisions, like an investment in IDBI Bank as the critics are pointing out, returns on LIC’s investment portfolio could suffer. That in turn would reduce the returns that it can generate for its policyholders. Ergo, it is unfair on the policyholders for LIC to be rescuing the government’s budget by picking up such sub-optimal investments.

Keeping aside the merits of the particular investment for a moment, the objection, purely at a headline conceptual level too, has merits. However, skinned one level below, it misses a crucial variable — 100% government ownership of LIC, which makes all claims on it essentially sovereign obligations. Once taken into account, much of the critique becomes theoretical rather than real.

LIC is an insurance company, and insurance policies that are bought can broadly be classified in three categories.

One, traditional insurance policies — these are primarily for protection, ie, protection of the immediate family due to the death of the policyholder. Some variants of these policies (variously known as Endowment or Money-back in India) involve return of premium paid/sum assured on maturity of the policy — returns are usually not guaranteed (though sometimes they are in certain policies) and are not the primary objective of the policy.

Two, unit-linked policies, or ULIPs. These are as much investment products as they are for protection, and the performance of ULIP is linked to financial markets — usually a mix of equity and fixed income.

Now, how is this relevant? It goes back to the essential point on “fairness”. Bulk of insurance policies sold by LIC comes under the first category above. What that means is that LIC is on the hook for committed liabilities — death claims, maturity proceeds and guaranteed returns — wherever applicable in terms of the respective policy features. Technically, the ability of LIC to fund these obligations is determined by the performance of its investment portfolio. Practically though, all these obligations are sovereign obligations of the Government of India (GOI). In a curious way, but effectively, it isn’t very different from GOI raising money via a bond issuance from the public and investing that money to (say) infuse capital into IDBI Bank. The primary difference is in the balance sheet treatment — a bond issuance by GOI would land up in the Union Budget, while fund infusion by LIC is “off budget” in nature. Not the best, most transparent way of doing things, but given various constraints, not an option that would kill. Irrespective of how the underlying portfolio performs, LIC (and by proxy, GOI) is liable to pay up the committed claims of policyholders. For policyholders, this means they have taken no more than sovereign risk — the highest quality credit risk that a domestic investor can invest in. The doomsday scenarios around betrayal of fiduciary trust that critics are panning the government for are more paper than reality.

Which leaves us with the last piece — ULIPs — where LIC’s role as a fund manager is as important as its role as a risk underwriter. It is here that inclusion of sub-optimal investments would fly against the grain of treating policyholders fairly, as policyholder returns are linked to performance of the underlying portfolios. To the extent of inclusion of (say) IDBI Bank, or any other disinvestment bailouts, result in lower returns in ULIPs, the critique is valid. The saving grace though is ULIPs form a relatively small part of total premia collected by LIC (~10-15%), and hence the impact of a few high-profile cases like IDBI Bank on the overall portfolio is marginal. However, it is a pertinent concern, and relevant regulator (IRDA) would need to take a look at the same. At the same time, competitive pressures on performance in ULIPs would ultimately be the best antidote to sub-par performance of LIC ULIPs.

There are seldom any perfect answers to tough choices in public policy-making, rescuing public sector banks in India is one such instance. Using LIC as a vehicle disturbs the purist, but perhaps only making the best of a tricky situation today.

The Indian Rupee (INR) is back in headline news. Thanks to a sharp upturn in global crude oil prices and an expansion in India’s current account deficit (CAD), INR has been under pressure for the last couple of months – depreciating against the US Dollar (USD) by ~5 per cent year till date. After a period of remarkable stability for three years, depreciation of INR has caused renewed flutter in the popular media over both the level of INR and how much it could depreciate by in the near future.

The issue though, cutting through the noise, is whether this is abnormal? Or is it merely a reversion to the normal? Is it something that is desirable? Or do policymakers (government, RBI etc) need to do something about it?

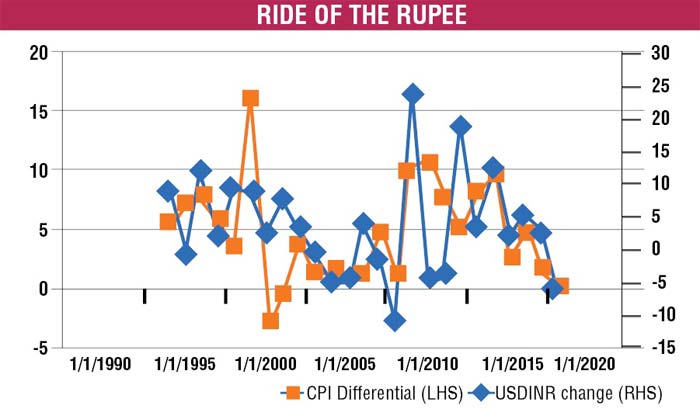

First things first, structurally, at the core of currency valuation, is the fact that appreciation (or depreciation) of a currency against another currency reflects the inflation differential between the two economies. Intuitively, this makes sense – if India runs an inflation of, say, 6 per cent, and the US runs an inflation of, say, 2 per cent, over the course of a year, a unit of Indian currency would be worth 4 per cent less than a unit of US currency. Over long periods of time, this relationship holds out as the chart shows.

There is nothing fundamentally wrong in a developing economy like India running a somewhat higher inflation than a developed market like the US. Ergo, a certain amount of currency depreciation is structurally built into India’s current development stage. So, what is there to panic about?

The issue, outside of a small group of people who conflate level of the currency with economic virility, isn’t with the depreciation per se, but the volatility associated with currency movements. INR, for example, gained against the USD in 2017 by 5-6 per cent. Now when it has shaved off all that gain in a matter of 2-3 months in 2018, a lot of market participants (and observers of the market) are getting worried. What they are really spooked by isn’t, therefore, the level of INR, but by the volatility associated with its price movements.

Is low volatility a good thing? The RBI has a stated policy of dampening the volatility of INR, without really determining a specific level of the currency. This is a practical stance in most parts as high volatility hurts the ability of operating businesses to adjust with the level of the currency. There is never a free lunch though, and RBI’s policy of keeping volatility low also leads to a build-up in market complacency. Since the “taper tantrum”-led crisis in 2013, there has been a large build-up in Foreign Portfolio Investor (FPI) holdings in Indian debt securities. A vast majority of these investments, $65-70 billion at last count, are the result of “carry trades”. In simple terms, FPI investors have invested this amount because of a) the large differential between the interest rates in India and the US and b) an assumption that INR will not be very volatile, and hence preserve the USD value of investments long enough for them to make a profit in USD terms. The second assumption is key and predicated on the assumption that there won’t be sudden, large depreciation in INR. Typically, such complacent assumptions by the market tend to result in excesses getting built into the system during good times, and driving up the underlying asset price (INR in this case) beyond the fair value of the asset. And when macro conditions turn for the worse, these excesses tend to be violently corrected, sometime leading to panic and disruptions.

This then begs the question: Is INR over-valued? Or fairly valued? The bellwether benchmark for estimating value of INR has been RBI’s Real Effective Exchange Rate (REER) Index. A level above 100 nominally represents INR to be overvalued, while a level below 100 would be undervalued. From a peak level of 121, the REER is hovering around 115-116 now. Which means that theoretically, INR is still overvalued. However, real life is seldom congruous to theory. There are multiple policy imperatives – a lower level of INR makes for more expensive imports, driving up inflation and, therefore, interest rates. On the other hand, it also reduces demand for imports, and allows domestic industry some headroom to replace the imports with locally manufactured substitutes. There are no easy answers, but on balance, the question of valuation is somewhat moot. What businesses and consumers are most affected by is shocks, rather than direction. If the natural direction of INR is to take it lower than its current levels, it shouldn’t be a policy imperative to stop its journey, but merely to regulate its spikes.

In the recent past, there have been radical solutions suggested – including a large FCNR(B) deposit raising by RBI, similar to the one done in 2013 – in order to shore up the currency. By most available indicators though, it is a call to action in order to be seen to be doing something, rather than something that is direly needed to be done. A falling INR isn’t a reflection of India’s economic strength, it merely recognises a financial reality. Neither panic nor complacency is an appropriate policy response.

Little excites policymaking commentary in India more than a debate on the size of government. Recently, a raft of government departments (Indian Railways, certain state police forces) announced large recruitment programmes – engendering another round of cautionary, even borderlineapocalyptic, prognosis on the immediate adverse impact on the economy.

As it is, for a government that had “minimum government” as a campaign slogan, a point usually made in popular commentary is how little the present government has done to cut what is described as a “bloated” public sector.

The impression has been further magnified by the absence of any major movement towards that touchstone of reform-achievement – privatisation.

The key question that is missed though is: do we have a “large, bloated” government as is constantly alleged? And is it the large size of the government that is dragging down efficiencies, resulting in sub-optimal economic outcomes? While there is no predictable benchmark of size of government and economic outcomes, it is useful to subject the popular hypotheses against available data.

On headline government spending as percentage of GDP, India, far from having an extraordinarily large government footprint, is actually an outlier on the other side – government expenditure contributes very little to GDP. A snapshot below gives the picture.

Further, the trend over the last decade shows that India has actually been squeezing down government expenditure as % of GDP, while the trend in most other countries has been a lot more expansionary. On top of headline expenditure, policymakers in India have internalised a bunch of buzzwords that have likely had adverse impact on outcomes — a definition of “revenue expenditure bad”, “capital expenditure good”. As a result we have a huge expansion of road networks without commensurate addition to municipal and road safety services, new schools/universities/institutions and significant investments in the physical upgradation of existing schools without a commensurate increase in the numbers (and quality) of teachers/administrative personnel, shiny new public hospitals in remote corners of India without enough doctors/nurses/sanitation workers. As a result, our outcomes on key human development metrics – education, healthcare, quality of life – seem to lag the investments being made in the areas.

The issue seems to be one of state capacity – the Indian state simply doesn’t have enough human capital bandwidth to provide its citizens with reasonable quality public services. Data on the numbers of public servants is sketchy, but there are enough indicators to hold the hypothesis up. The 7th Pay Commission (SPC) report gives comparative numbers of the numbers of public servants in India and US, another large country with a federal political structure. Total number of civilian non-postal/railways Central Government employees in India (in 2014) is around 18 lac. The comparative number for Federal employees in the US is 21 lac. Adjusted for population, the difference is stark – for every lac of population, India has a total of 139 Central government employees, while the comparative number for the US is 668.

Adding in state government and local bodies too, from the Labour Ministry Statistical Handbook, the numbers move up significantly, but still short of comparable international standards.

The best concentration of public servants (as percentage of population) are in remote hilly and border states, besides insurgency-prone regions – these are states where there are special funding programmes from the Central government to increase state capacities to deal with insurgency, border management and geographic remoteness. So Himachal Pradesh has 3,700 public servants for every lac of population, while Manipur, Tripura and Nagaland are all in the 3,000-3,500 range. Even these exceptionally elevated numbers are far short of comparable international levels. For the vast majority of states though, including comparatively richer states like Gujarat, Maharashtra and Haryana, the numbers hover between 1,000 and 1,300 for every lac of population. While there are no empirical studies on causality between delivery outcomes of public services and numbers of public servants – the numbers do indicate a serious dearth of state capacity, which perhaps explains why even the more prosperous states are struggling to meet key human development goals.

The rhetoric of “large government” constrains India when our gaps in service outcomes on a range of social and economic indicators. The Indian state gives the impression of being all pervasive without the capacity to deliver a fraction of its optical presence (and promise). Further cutbacks in the size of the Indian state would only exacerbate our relative deficiencies against the rest of the world. Its time that the India state grew bigger, and not smaller, while citizens demand more accountability from the larger state capacities. The popular rhetoric notwithstanding.