Media reports of the government offloading a substantial chunk of its shareholding in IDBI Bank to Life Insurance Corporation of India (LIC) has sparked off another round of passionate debate on the appropriateness of the action. To be sure, LIC has been an equity investor of last resort for the government for many years — periodically picking up the slack in capital market sentiments for the government’s interventions. Primarily, this has been around the disinvestment programme, with LIC consistently bailing out share sales in PSUs with lukewarm investor interest (a recent case in point being the Hindustan Aeronautics Ltd (HAL) IPO).

One objection to this has been a purists’ lament around whether such share sale really means “disinvestment” of government equity. However, the bigger and arguably a more pertinent point is around whether LIC is being amiss in its fiduciary responsibility as an insurer by deploying capital in sub-par investments, just to bail out the government. IDBI Bank, with its stressed balance sheet (28% gross NPA), is symptomatic of such “subpar investments”. The latter argument has strong merit — the capital available with LIC is essentially premia paid by its policyholders. LIC invests this capital in order to generate enough surpluses to fund claims, death benefits and maturity proceeds to policyholders and their beneficiaries. To the extent LIC makes sub-optimal investment decisions, like an investment in IDBI Bank as the critics are pointing out, returns on LIC’s investment portfolio could suffer. That in turn would reduce the returns that it can generate for its policyholders. Ergo, it is unfair on the policyholders for LIC to be rescuing the government’s budget by picking up such sub-optimal investments.

Keeping aside the merits of the particular investment for a moment, the objection, purely at a headline conceptual level too, has merits. However, skinned one level below, it misses a crucial variable — 100% government ownership of LIC, which makes all claims on it essentially sovereign obligations. Once taken into account, much of the critique becomes theoretical rather than real.

LIC is an insurance company, and insurance policies that are bought can broadly be classified in three categories.

One, traditional insurance policies — these are primarily for protection, ie, protection of the immediate family due to the death of the policyholder. Some variants of these policies (variously known as Endowment or Money-back in India) involve return of premium paid/sum assured on maturity of the policy — returns are usually not guaranteed (though sometimes they are in certain policies) and are not the primary objective of the policy.

Two, unit-linked policies, or ULIPs. These are as much investment products as they are for protection, and the performance of ULIP is linked to financial markets — usually a mix of equity and fixed income.

Now, how is this relevant? It goes back to the essential point on “fairness”. Bulk of insurance policies sold by LIC comes under the first category above. What that means is that LIC is on the hook for committed liabilities — death claims, maturity proceeds and guaranteed returns — wherever applicable in terms of the respective policy features. Technically, the ability of LIC to fund these obligations is determined by the performance of its investment portfolio. Practically though, all these obligations are sovereign obligations of the Government of India (GOI). In a curious way, but effectively, it isn’t very different from GOI raising money via a bond issuance from the public and investing that money to (say) infuse capital into IDBI Bank. The primary difference is in the balance sheet treatment — a bond issuance by GOI would land up in the Union Budget, while fund infusion by LIC is “off budget” in nature. Not the best, most transparent way of doing things, but given various constraints, not an option that would kill. Irrespective of how the underlying portfolio performs, LIC (and by proxy, GOI) is liable to pay up the committed claims of policyholders. For policyholders, this means they have taken no more than sovereign risk — the highest quality credit risk that a domestic investor can invest in. The doomsday scenarios around betrayal of fiduciary trust that critics are panning the government for are more paper than reality.

Which leaves us with the last piece — ULIPs — where LIC’s role as a fund manager is as important as its role as a risk underwriter. It is here that inclusion of sub-optimal investments would fly against the grain of treating policyholders fairly, as policyholder returns are linked to performance of the underlying portfolios. To the extent of inclusion of (say) IDBI Bank, or any other disinvestment bailouts, result in lower returns in ULIPs, the critique is valid. The saving grace though is ULIPs form a relatively small part of total premia collected by LIC (~10-15%), and hence the impact of a few high-profile cases like IDBI Bank on the overall portfolio is marginal. However, it is a pertinent concern, and relevant regulator (IRDA) would need to take a look at the same. At the same time, competitive pressures on performance in ULIPs would ultimately be the best antidote to sub-par performance of LIC ULIPs.

There are seldom any perfect answers to tough choices in public policy-making, rescuing public sector banks in India is one such instance. Using LIC as a vehicle disturbs the purist, but perhaps only making the best of a tricky situation today.

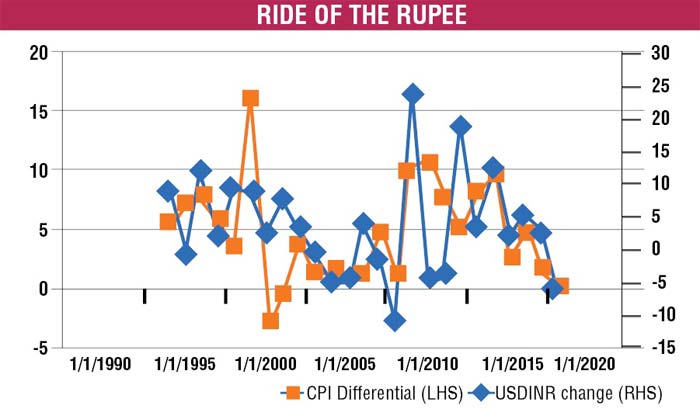

The Indian Rupee (INR) is back in headline news. Thanks to a sharp upturn in global crude oil prices and an expansion in India’s current account deficit (CAD), INR has been under pressure for the last couple of months – depreciating against the US Dollar (USD) by ~5 per cent year till date. After a period of remarkable stability for three years, depreciation of INR has caused renewed flutter in the popular media over both the level of INR and how much it could depreciate by in the near future.

The issue though, cutting through the noise, is whether this is abnormal? Or is it merely a reversion to the normal? Is it something that is desirable? Or do policymakers (government, RBI etc) need to do something about it?

First things first, structurally, at the core of currency valuation, is the fact that appreciation (or depreciation) of a currency against another currency reflects the inflation differential between the two economies. Intuitively, this makes sense – if India runs an inflation of, say, 6 per cent, and the US runs an inflation of, say, 2 per cent, over the course of a year, a unit of Indian currency would be worth 4 per cent less than a unit of US currency. Over long periods of time, this relationship holds out as the chart shows.

There is nothing fundamentally wrong in a developing economy like India running a somewhat higher inflation than a developed market like the US. Ergo, a certain amount of currency depreciation is structurally built into India’s current development stage. So, what is there to panic about?

The issue, outside of a small group of people who conflate level of the currency with economic virility, isn’t with the depreciation per se, but the volatility associated with currency movements. INR, for example, gained against the USD in 2017 by 5-6 per cent. Now when it has shaved off all that gain in a matter of 2-3 months in 2018, a lot of market participants (and observers of the market) are getting worried. What they are really spooked by isn’t, therefore, the level of INR, but by the volatility associated with its price movements.

Is low volatility a good thing? The RBI has a stated policy of dampening the volatility of INR, without really determining a specific level of the currency. This is a practical stance in most parts as high volatility hurts the ability of operating businesses to adjust with the level of the currency. There is never a free lunch though, and RBI’s policy of keeping volatility low also leads to a build-up in market complacency. Since the “taper tantrum”-led crisis in 2013, there has been a large build-up in Foreign Portfolio Investor (FPI) holdings in Indian debt securities. A vast majority of these investments, $65-70 billion at last count, are the result of “carry trades”. In simple terms, FPI investors have invested this amount because of a) the large differential between the interest rates in India and the US and b) an assumption that INR will not be very volatile, and hence preserve the USD value of investments long enough for them to make a profit in USD terms. The second assumption is key and predicated on the assumption that there won’t be sudden, large depreciation in INR. Typically, such complacent assumptions by the market tend to result in excesses getting built into the system during good times, and driving up the underlying asset price (INR in this case) beyond the fair value of the asset. And when macro conditions turn for the worse, these excesses tend to be violently corrected, sometime leading to panic and disruptions.

This then begs the question: Is INR over-valued? Or fairly valued? The bellwether benchmark for estimating value of INR has been RBI’s Real Effective Exchange Rate (REER) Index. A level above 100 nominally represents INR to be overvalued, while a level below 100 would be undervalued. From a peak level of 121, the REER is hovering around 115-116 now. Which means that theoretically, INR is still overvalued. However, real life is seldom congruous to theory. There are multiple policy imperatives – a lower level of INR makes for more expensive imports, driving up inflation and, therefore, interest rates. On the other hand, it also reduces demand for imports, and allows domestic industry some headroom to replace the imports with locally manufactured substitutes. There are no easy answers, but on balance, the question of valuation is somewhat moot. What businesses and consumers are most affected by is shocks, rather than direction. If the natural direction of INR is to take it lower than its current levels, it shouldn’t be a policy imperative to stop its journey, but merely to regulate its spikes.

In the recent past, there have been radical solutions suggested – including a large FCNR(B) deposit raising by RBI, similar to the one done in 2013 – in order to shore up the currency. By most available indicators though, it is a call to action in order to be seen to be doing something, rather than something that is direly needed to be done. A falling INR isn’t a reflection of India’s economic strength, it merely recognises a financial reality. Neither panic nor complacency is an appropriate policy response.

Little excites policymaking commentary in India more than a debate on the size of government. Recently, a raft of government departments (Indian Railways, certain state police forces) announced large recruitment programmes – engendering another round of cautionary, even borderlineapocalyptic, prognosis on the immediate adverse impact on the economy.

As it is, for a government that had “minimum government” as a campaign slogan, a point usually made in popular commentary is how little the present government has done to cut what is described as a “bloated” public sector.

The impression has been further magnified by the absence of any major movement towards that touchstone of reform-achievement – privatisation.

The key question that is missed though is: do we have a “large, bloated” government as is constantly alleged? And is it the large size of the government that is dragging down efficiencies, resulting in sub-optimal economic outcomes? While there is no predictable benchmark of size of government and economic outcomes, it is useful to subject the popular hypotheses against available data.

On headline government spending as percentage of GDP, India, far from having an extraordinarily large government footprint, is actually an outlier on the other side – government expenditure contributes very little to GDP. A snapshot below gives the picture.

Further, the trend over the last decade shows that India has actually been squeezing down government expenditure as % of GDP, while the trend in most other countries has been a lot more expansionary. On top of headline expenditure, policymakers in India have internalised a bunch of buzzwords that have likely had adverse impact on outcomes — a definition of “revenue expenditure bad”, “capital expenditure good”. As a result we have a huge expansion of road networks without commensurate addition to municipal and road safety services, new schools/universities/institutions and significant investments in the physical upgradation of existing schools without a commensurate increase in the numbers (and quality) of teachers/administrative personnel, shiny new public hospitals in remote corners of India without enough doctors/nurses/sanitation workers. As a result, our outcomes on key human development metrics – education, healthcare, quality of life – seem to lag the investments being made in the areas.

The issue seems to be one of state capacity – the Indian state simply doesn’t have enough human capital bandwidth to provide its citizens with reasonable quality public services. Data on the numbers of public servants is sketchy, but there are enough indicators to hold the hypothesis up. The 7th Pay Commission (SPC) report gives comparative numbers of the numbers of public servants in India and US, another large country with a federal political structure. Total number of civilian non-postal/railways Central Government employees in India (in 2014) is around 18 lac. The comparative number for Federal employees in the US is 21 lac. Adjusted for population, the difference is stark – for every lac of population, India has a total of 139 Central government employees, while the comparative number for the US is 668.

Adding in state government and local bodies too, from the Labour Ministry Statistical Handbook, the numbers move up significantly, but still short of comparable international standards.

The best concentration of public servants (as percentage of population) are in remote hilly and border states, besides insurgency-prone regions – these are states where there are special funding programmes from the Central government to increase state capacities to deal with insurgency, border management and geographic remoteness. So Himachal Pradesh has 3,700 public servants for every lac of population, while Manipur, Tripura and Nagaland are all in the 3,000-3,500 range. Even these exceptionally elevated numbers are far short of comparable international levels. For the vast majority of states though, including comparatively richer states like Gujarat, Maharashtra and Haryana, the numbers hover between 1,000 and 1,300 for every lac of population. While there are no empirical studies on causality between delivery outcomes of public services and numbers of public servants – the numbers do indicate a serious dearth of state capacity, which perhaps explains why even the more prosperous states are struggling to meet key human development goals.

The rhetoric of “large government” constrains India when our gaps in service outcomes on a range of social and economic indicators. The Indian state gives the impression of being all pervasive without the capacity to deliver a fraction of its optical presence (and promise). Further cutbacks in the size of the Indian state would only exacerbate our relative deficiencies against the rest of the world. Its time that the India state grew bigger, and not smaller, while citizens demand more accountability from the larger state capacities. The popular rhetoric notwithstanding.

Cryptocurrencies have captured the imagination of a section of investors globally. An idea with seductive appeal — cryptocurrencies (like Bitcoins) have gained both fame and notoriety, leading to a global regulatory weariness around them. The latest sceptic is the Reserve Bank of India, which recently banned regulated entities from dealing in cryptocurrencies in India. While commercial, private cryptos struggle with extreme price volatility and regulatory scepticism, there is another interesting concept being developed globally — one of Central Bank Digital Currency (CBDC). In a nutshell, can RBI issue a digital currency, lets call it the BharatCoin, just as it issues currency notes today? It’s an idea whose time has come, and there are some compelling reasons why RBI should consider issuing BharatCoins.

The most important application of BharatCoin would be to provide the general public an expansion in choice for a deposit account – it would be akin to an online-only, sovereign-risk bank account with a modern and cheap payment option. BharatCoin would provide safety of the sovereign like in currency notes (it would be a liability of RBI, in effect the Government of India, rather than a bank), likely provide an interest unlike currency notes today (which are zero interest-bearing instruments, and holders get no return for storing them in their wallets), would be cheaper than most electronic payment solutions today, and have the ability to transact anywhere and with anyone with access to a smartphone. At the same time, for RBI, it would be infinitely cheaper to issue BharatCoin in a digital format than to print, transport, safeguard and carry out forensics on counterfeits on currency notes today. The savings from this exercise would accrue to RBI, and by definition, to the taxpayer.

Second, BharatCoin could make the process of monetary policy transmission lot smoother and efficient. RBI influences monetary policy via changes in what is commonly called “policy rates”— these are rates at which RBI borrows from (or lends to) approved counterparties. However, the list of approved counterparties to RBI is quite small, consisting primarily of licensed banks. Therefore, the transmission of a rate cut (or hike) by RBI to the public (and corporations) at large is dependent on a small set of banks faithfully transmitting the same. For obvious reasons, this is often prone to issues, especially if the small set of counterparties collude with each other to minimise the transmission. It’s an issue that RBI has often raised concerns over. BharatCoin dramatically increases the number of approved counterparties to RBI —essentially anyone holding a BharatCoin is a counterparty — in effect millions of retail and corporates who hold BharatCoin instead of cash or bank deposits. If RBI (say) raises policy rates, and banks refuse to pass on the entire rate hike to depositors, millions of depositors would have an option to en masse swap their deposits for BharatCoins, thereby exerting competitive pressure on banks to follow suit quickly. A more efficient transmission of monetary policy would typically result in better all-round outcomes on economic development, as RBI can sharpen its interventions and minimise collateral impact.

Third, BharatCoin will enable the RBI potentially minimise the cost of government debt. The primary source of revenues for any central bank (including RBI) is issuance of currency notes. For every (say ₹100) note that RBI issues, it holds an equivalent amount of government bond in its balance sheet. As RBI pays no interest on a currency note, it makes the spread between the yield on the government bond it holds and the zero interest rate it pays on the currency note — in technical terms, called seigniorage. Earnings from seigniorage accrues to GOI, which is used for either tax-cuts or spends on various development activities. As the economy starts using less cash at the margin, there is potentially a risk to seigniorage revenues. BharatCoin issuance would be a potential hedge against such a possibility, as issuance of BharatCoins would be similar to that of currency notes, ie, against RBI holdings of government bonds, and accrue seigniorage revenues. In a recent paper on CBDC, Bank of England estimated a 3% boost to GDP on account of interest set-offs to government debt made possible via issuance of CBDC.

Last, but not the least, BharatCoin resolves an old monetary policy conundrum of “zero lower bound”. If RBI needs to reduce policy rates to negative levels in response to a severe slowdown, the existence of cash obstructs the slide below zero. With RBI policy rates at (say) -2% and currency notes yielding 0%, authorised counterparties like banks will convert their reserves with RBI en masse into cash until only the latter remains. At this point RBI would have lost its ability to reduce rates — cash doesn’t pay interest nor can it be penalised — and would no longer be capable of exercising monetary policy. This is the zero-lower bound.

BharatCoin can solve the problem. As it gains more acceptance among the general public in lieu of cash, RBI can cancel high denomination notes. Consequently, in a crisis situation, RBI would have the flexibility of taking policy rates down to negative levels. If authorised counterparties like banks wanted to convert RBI reserves into BharatCoin, the rates on the latter too can be brought down to similar negative levels. Sans high denomination currency notes, the option of converting to cash becomes impractical from a storage/security/warehousing perspective. In a nutshell, it gives greater flexibility to RBI to pursue unconventional monetary policies should the economic situation warrant. Not a situation that India faces in the immediate future, but given the experience of developed economies in the last few years, it provides a template to be prepared!

The flip side? It would be increased competition for banks on their most valuable franchise — retail deposits. Interestyielding BharatCoin would be everything that a bank deposit is, without the credit risk inherent in a bank, and transaction costs that are likely to be a fraction of what banks charge.

BharatCoin will not be a perfect substitute for cash, especially around the privacy features of the latter. However, it is a concept that bears immense promise – of disruption in financial markets and a sharper, better way of administering monetary policy.

India is finally grappling seriously with its large non-performing assets (NPA) problem, and the first green shoots of structural changes — recapitalisation, new bankruptcy code, and new NPA recognition norms to resolve the issue — are seemingly visible. While the new institutions, laws and regulations will learn as they are tested, there is a belief that the problem is closer to resolution than ever before in the last four years. However, this is merely rectifying the past.

An equally tricky issue, one that has received somewhat less attention is: What next? How would we fund the next investment cycle which should be taking off in the next year or two? The present NPA crisis was substantially engendered by commercial banks funding infrastructure and other long-term capital expenditure in a big way. It is unlikely that either shareholders, including the government, or the regulator (RBI) would be overly enthusiastic to have commercial banks funding long-term infrastructure again in a big way. Which begs the question, how does India fund its enormous infrastructure needs? Over the last few years, alternate modes of financing — Non-Banking Finance Companies (NBFC), Mutual Funds (MF) and Alternative Investment Funds (AIF) have grown in size and appetite to fund long-term financing requirements. However, structurally MFs and other instruments are largely open-ended vehicles with limited appetite for long-term, illiquid assets. As a result, in terms of size, they are going to be insufficient to bridge the gap that will be left by banks.

In a typically karmic twist, it would seem that the solution would lie in the resurrection of Development Finance Institutions (DFI). Till about 20 years ago, long-term capital requirements of the Indian corporate sector were met by DFIs. The raison d’être of DFI financing long-term debt capital was quite intuitive. DFIs would typically raise long-term financing via attractive tax-free bonds, making it possible to extend long-term loans without running into huge asset-liability mismatch issues. Universal Commercial Banks (UCB), on the other hand, typically raise funding via short-term deposits, and used to have very high statutory liquidity requirements in the forms of Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR). Consequently, it was quite unviable, both from a pricing as well as from a risk management perspective, for UCB to do large-scale long-term financing.

However, liberalisation changed the landscape completely. With reforms, came in a substantial decrease in CRR and SLR, thereby drastically reducing the cost of funding for UCB. Consequently, the pricing advantage on the cost of funds is reversed, with UCB having a large advantage over DFI. Further, liberalisation of financial markets brought in new instruments (like Interest Rate Swaps, MIFOR, etc) that participants could see developing into effective hedging tools for asset-liability mismatches (long-term loans, short-term, funding via deposits) in the foreseeable future. Liberalisation also brought around an expansion of market participants in the form of mutual funds and private sector insurance companies, both of whom were expected to broaden the market for the new instruments. Soon enough, two of the largest DFIs (ICICI and IDBI) mutated into universal commercial banks, while two others (IFCI and IRBI) withered away.

Unfortunately, as we have seen over the last few years, UCB’s foray into long-term lending has not been a happy experience. Given that most UCBs are funded to a large extent by retail deposits, it has also meant a default sovereign guarantee on the UCB, resulting in taxpayer-funded bailouts. While these are much smaller than the rest of the world, it still raises questions of fairness and accountability.

Ironically, DFIs would be an interesting solution to the problem. They could be primarily funded by wholesale customers through deposits or bonds issued to large corporates and institutions. Ergo, there would be lesser pressure on the government to intervene even if there is a viability issue that develops. Second, being focused on long-term loans, DFIs would develop unique skill-sets in assessing, underwriting and managing their risks. The RBI issued a discussion paper on wholesale and long-term finance banks last year on the viability of a similar construct. It would be tough to revert to the pre-1991 construct of DFI — the world has changed, and Indian markets have also gotten a lot more sophisticated.

The DFI, in its new avatar, could be a hybrid between a western-style investment bank and a traditional UCB. It would not only raise long-term financing to fund long-term assets, it would also be an active market participant in developing the long-term corporate bond market. Contrary to popular notions, India does not have a shallow corporate bond market compared to other peer-group economies in the developing world.

The issue is one of secondary-market liquidity, caused by a dearth of market participants in the space. The new DFI would be an active market-maker in long-term financing structures, as an intermediary as well as a source of intellectual capital. India has been actively scouting for and in some ways successfully attracting foreign investment pools like pension funds and sovereign wealth funds for infrastructure investments. However, given the magnitude of our requirements, foreign investment will always be a small complement to the domestic effort. We need institutions with long-term asset-liability horizons to fund India’s infrastructure, and re-engineered and imagined DFIs are a uniquely suitable option. It’s an idea whose time has come because without an alternative mechanism, India’s long-term financing needs will be hobbled.

“Plus ça change, plus c’est la même chose” — the more things change, the more they remain the same. The old chestnut seems amazingly prescient for India’s banking market!

The PNB scam has ratcheted up the decibel levels of the debate around public sector banks (PSBs) in India. Unfortunately, the debate has been primarily focused around the ownership structure of the banks – publicly owned. It’s somewhat Kafka-esque – obsessing about black coffee after being beaten senseless by a couple of goons (Amerika, Franz Kafka’s first novel)! When the debate should be, as has been the case in the West for some time, about the role of banks per se.

In simple terms, are banks meant to be turbo-charged return on equity (ROE) machines, driving innovation, risk-taking and high returns for shareholders? Or should they be public utilities meant to provide low-risk plumbing for the real economy, not blowing up, and if they do, not presenting catastrophic outcomes for society? The question has always been around banking, but the question has become centre-of-plate since the financial crisis in 2008. At the core is the realisation that banking losses, irrespective of the nature of ownership, is a public liability.

Higher capital requirements under Basel III, higher compliance requirements, stripping off risky parts of banking from universal banks – there has been a global attempt towards making banks closer to utilities than ever before. In short, convert TBTF to “Too Boring To Fail” from “Too Big To Fail”. In many ways, the impact is visible – with ROEs of banks globally more resembling utilities (5-9%) than banking in the previous decade (15-20%).

Unfortunately, the debate in India gives this a near-complete miss. In some ways, the so-called “reforms” are looking to reverse the better characteristics of Indian banking.

To start with, the assumption of big being better. For many years now, the government has postulated that most PSBs are too small, and need to be merged into larger, “global sized” banks. While progress on this front has been slow, SBI did a mega merger of all its associate banks last year as part of the same strategy. It’s a strange hypothesis – smaller the bank, smaller would be its organic and systemic impact of failure. India is uniquely blessed in this regard – barring SBI and ICICI, most banks have single-digit market shares. It makes the system more resistant to systemic failures. But proposed “reforms” are looking to create a more vulnerable banking system by creating larger banks.

Second, while there is a welcome new process/law for bad loan resolution, there is still little work on addressing the core issues. Banking loans fall essentially under three categories – corporate finance, corporate and commercial loans and retail loans. In India, bulk of NPA issues have arisen on account of large project finance loans extended by PSBs. Earlier, the failure of Global Trust Bank was on account of large exposure to capital markets. There is a fundamental mismatch – between the riskappetite and tenor of the liability (deposits) and asset (loans) sides of the banks’ balance sheets here. Unfortunately, even as RBI (and the government) have tightened operational rules around lending, credit appraisal etc, there has not been any serious discussion around why commercial banks, funded by short-term retail deposits, should be giving out long-term project loans, or write guarantees secured by capital market exposures.

Third, India has gone slow on capital buffers. Even as GOI embarks on a massive recapitalisation plan for PSBs, amounting to over ₹2 lakh crore, there is little conversation on how and why Indian banks would continue to have weaker equity capital buffers compared to the rest of the world.

Corporate finance activities should be done from an entity outside of a commercial bank. They should not be allowed to be funded by retail deposits. Two, banks that raise bulk of their deposits from retail customers should be restricted to writing retail and selective corporate & commercial loans. Balance corporate/commercial loans should be funded out of deposits raised from wholesale (corporations, institutions etc) customers. Three, capital requirements on banks should be set high, so high that they simply cannot fail. Once done, there would be little probability of taxpayer bailouts, irrespective of ownership.

The debate on ownership, especially privatisation, is sexier than a debate around the social contract of banking. As it was for Karl Rossman in Amerika, it was more interesting to discuss the role of black coffee in his station in life, rather than the tragedy of his journey from Europe to New York. But banking might require a touch more attention than Kafka!

Earlier this month, the three largest stock exchanges in the country — National Stock Exchange (NSE), Bombay Stock Exchange (BSE) and the new Metropolitan Stock Exchange (MSE) — agreed to stop sharing data with overseas stock exchanges that offer derivative contracts linked to popular Indian indices and stocks. As soon as the news hit the wires, the predictable responses came out like the proverbial ants out of the woodworks — it’s anti-competitive, a policy self-goal, protectionist. MSCI, the popular global index-provider, even darkly hinted at a possible cut in India’s weightage in its global benchmark indices.

The fact though is, from the perspective of the Indian stock exchanges, this was a perfectly sensible competitive move. It made so much sense that two intensely competitive companies — NSE and BSE fight a bruising battle for market share and market access — came together on this issue. This move is simply a way for Indian bourses to protect their own market share from a steady haemorrhage. The rationale is pretty simple.

NSE, BSE today share, with a range of offshore stock exchanges, price feeds and index brands for stocks and popular benchmark indices listed on their platforms. These offshore bourses — primarily in Singapore, Dubai and Hong Kong — in turn use the price feeds and brands to float their own India products — SGX Nifty for example. Over the last few years, a significant amount of incremental trading on Indian indices have moved to these offshore platforms. Reasons are manifold, lower taxes for one — Singapore/Hong Kong/Dubai do not have taxes on capital gains made out of derivative contracts, unlike India. Severe restrictions in India on Participatory Notes (P-Notes), a popular instrument used by a variety of foreign investors to take equity exposures are a second. Above all, there is also the ease of regulatory environment, where many of these offshore markets are considered better than India. The proverbial last straw in the camel’s back was the launch of 50 Indian single stock futures by SGX earlier this month.

NSE and BSE came together to essentially use the nuclear option, ie, access to price feeds. Sans access to price feeds (as also brand rights to the popular indices, though that is a smaller issue), the ability of traders on the SGX (or any other offshore exchange) platform to efficiently price Indian underlying products is severely impaired. It also required both BSE and NSE to cooperate on the issue, as restriction by only one of the two would keep the window of price feeds open from the other, and defeat the purpose altogether. In other words, it’s a question of pure self-interest in a competitive market, where offshore exchanges like SGX were actively competing with BSE/NSE for market share. Nothing “protectionist” about it at all. The fact that SGX’s own share price fell 9 per cent on the day the announcement by BSE/NSE came partially reflects the competitive impact of this move.

How does this play out now for markets and its shape? In the short run, there’s unlikely to be any great impact. India hasn’t put physical controls over foreign access to Indian stock markets. India’s attractiveness as an investment destination too doesn’t change, one way or another, by the decision of local exchanges to either share or not share price feeds with their overseas counterparts. If investors and investment themes do not materially change, chances of index providers cutting India weightages are extremely remote too.

In the slightly longer run though, this would likely be a case of delaying the inevitable. The case of currency trading is illustrative in this respect. USDINR, the most popular currency pair traded on India, are traded both in India as well as offshore (in what is called the NDF — Non Deliverable Forward — market). Volumes in the NDF market are over twice the volumes traded onshore in India. This, despite the fact that the NDF market has structural limitations in the form of inability to “physically settle” trades, given that INR is not a convertible currency. Reasons are all familiar, and similar to the ones described for stocks above. Now, currency markets are largely OTC (Over The Counter — bilateral deals struck on the phone/computer network by two traders), and not exchange-traded, and hence do not require proprietary price feeds from an exchange, unlike equities. As a result, offshore traders cannot replicate the same model easily for equities.

There is also the additional factor of India’s own IFSC (International Financial Services Centre), in GIFT City, Gujarat. There’s been a huge amount of regulatory nudge to shift offshore trades there from overseas exchanges.

However, financial innovation typically tends to trump physical barriers. While its more difficult to price offshore-listed Indian derivatives sans data from NSE/BSE, its not impossible. There would be smart structures/traders/algorithm-writers at work to develop new models to obviate the issue. Given the experience worldwide, especially on USDINR case, it is a problem that doesn’t seem immune to being cracked. On IFSC, while taxes are somewhat lower compared to onshore exchanges, the issues around acceptability, ecosystem and market depth are still open questions for foreign investors to move serious volumes, yet.

Net-net, while the popular narrative around protectionism is widely misplaced, and this buys some time for India’s local exchanges, this is likely to look a bit more of Don Quixote than Napoleon in the longer run!

Bitcoin has assumed cult proportions, and naysayers in both financial markets (through their dire warnings of a Dutch Tulip redux) and global governments (through pre-emptive executive actions) have not really been able to fully dampen the enthusiasm of cult-followers. The real question though is if Bitcoin would be ever able to transcend its cult-status into its promised nirvana, ie, an alternative global currency. Prospects of that happening, while enormous challenges remain, are perhaps not the in “not in my lifetime” domain. Why? Let us examine the key hot buttons — demand and supply considerations of an alternative global currency.

Starting with demand — is there a demand for an alternative global currency? This is an easy answer — it is a loud, unambiguous YES. There are multiple intellectual convincing and politically powerful support for Bitcoins as an alternate currency.

First, the current international financial system is predicated on the status of US Dollar (USD) as the de facto reserve currency. Bulk of trade settlements, capital flows and money transfers happen in USD — giving the US government supranational powers to regulate the international financial system. Along with USD as the reserve currency, the entire global financial architecture is run by financial institutions around US rules. This gives enormous political powers to the US government — it can (and has) try to influence behaviour of people, corporations, even countries, by sanctioning their access to the global financial system. States at the receiving end of such action — Russia, Iran, Venezuela come immediately in recent memory — have enormous interest in breaking out of the straightjacket of USD. Bitcoin, where custody, transfer and trust are ensured by a disaggregated, decentralized protocol (rather than US laws), reduces the leverage of sanctions today that US government has.

Second, the crisis of confidence in the traditional monetary regime. Under the traditional monetary policy, new money is primarily created by “fiat”, or by central banks (representing their respective sovereign governments) printing money. Post the global financial crisis in 2008, central banks around the world used this power to print very large sums of money (popularly described as Quantitative Easing), with the objective to keeping interest rates low, finance government buy-outs of toxic financial assets, and give a general “monetary boost” to a crisis-hit global economy. In some parts, it worked. But it also left in its wake a crisis of confidence with a section of thought-leaders — as currency as an asset was seen to have been devalued by printing such large amounts, opening up possibilities of run-away inflation in the future.

Next, what about supply? Is Bitcoin (and the whole family of cryptocurrencies at large) geared up to become an alternative form of money? Any form of money has two features — as a medium of exchange and as a store of value. At an overarching level, money also has to support business cycles in the real economy.

As a medium of exchange, Bitcoin (and cryptocurrencies in general) shows the maximum promise — as a decentralised, public architecture — since money transfers can be done faster, cheaper and without taking credit risk on various intermediaries along the chain. A typical international wire transfer today navigates its way through multiple banks, clearing houses, custodians and transfer protocols (like SWIFT) — takes several days, with the only beneficiary being the intermediary banks making money out of the idle float. Cryptocurrencies like Litecoin can do the transfer in minutes, and cost virtually nothing.

The real issue with Bitcoin today though, is as a store of value. Rather, as a “stable” store of value. Volatility in Bitcoins today is very high, 20-25 times the volatility of stocks. Now, no one would generally like to be paid in a form of money that can be worth 15 per cent more (or less) the day after. Part of this is growing up pangs, Bitcoins do not have the normal full suite of financial products underlying the asset — most financial assets that do not have well-traded option contracts tend to be non-ergodic (in simple terms, subject to massive blow-ups). Recently, mainstream exchanges like Chicago Board of Trade and Chicago Mercantile Exchange started offering futures contracts on Bitcoins. Its not enough, futures contracts, sans a large, liquid options market, will not bring volatility down markedly. The point though is, this is just the beginning. Moore’s Law in financial market innovation will kick-in at some stage, especially with mainstream financial market participation increasing, and newer derivative instruments would start trading off Bitcoin underlyings. However, this is the toughest condition for Bitcoin to achieve for it to become a form of money.

Which brings us to the last issue, does Bitcoin lend itself to viable monetary policy formulation, one that can support the real economy? The first objection would be in terms of its finite quantity – Bitcoin is limited to 21 million. In times of economic downturn, it limits the ability of governments to expand the money supply to tackle the same. This isn’t as such a difficult problem, as Bitcoin is but one of many cryptocurrencies, there are many more (like Litecoin, Dash etc).

The bigger issue, though, is around the power of the State associated with money. Fiat money today is printed by governments, it’s a sovereign obligation. How would states react to a new architecture stripping that power away?

Philosophically, this would be the biggest supply-side question that Bitcoin has to answer. Good news (for Bitcoin fans), is that there is a modern precedent. About 500 million citizens in dozens of States, gave up their sovereignty to print money to a common shared pool — the European Monetary Union, on January 1, 1999 — giving birth to Euro. Some of the objectives of the Euro are not very dissimilar to the demand-side arguments for Bitcoin. In a nutshell, it has happened before! While the obstacles are many, so it would seem are the arguments in favour of Bitcoin. How the cookie crumbles would be an interesting story of our lifetime!